Quantum-Augmented Risk Management

for Capital Markets

A working two-stream classical architecture, deployable now — multifractal mathematics and bounded LLM orchestration — deliberately structured to intercept a research-stage third stream, quantum compute, at the single point where it would add value.

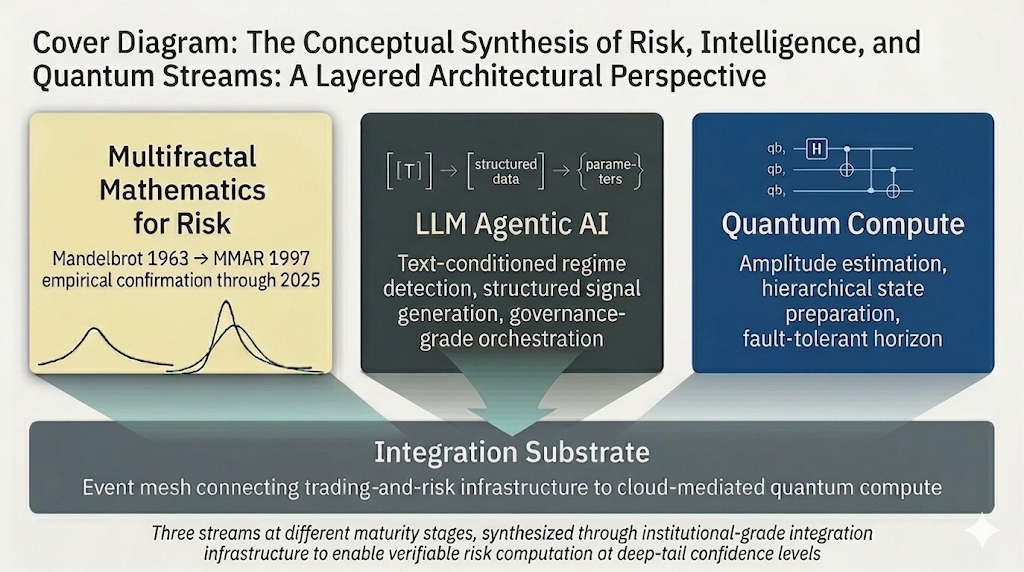

Three streams, asymmetric maturity.

Capital markets risk models overwhelmingly assume Gaussian or near-Gaussian returns, while six decades of evidence — beginning with Mandelbrot (1963) — show returns are fat-tailed, long-memory, and regime-dependent. The mismatch matters most exactly where risk matters most: at the deep tail, where capital adequacy and systemic resilience are actually decided. This architecture addresses that mismatch by synthesizing three streams that stand at different stages of maturity — and treating that asymmetry as the design, not an inconvenience.

Multifractal mathematics

The Multifractal Model of Asset Returns (Mandelbrot, Fisher, Calvet 1997) builds a loss distribution through a recursive multiplicative cascade. Its empirical contribution is concentrated at the deep tail: at VaR 95% Gaussian and multifractal models often agree; at VaR 99%+ the cascade captures probability mass Gaussian models systematically miss.

Rough volatility leads on vol-surface fitting and option pricing; on deep-tail VaR/ES the cascade family — in its forecasting-grade Markov-switching form — remains competitive to dominant, and the roughness-versus-multifractal question is itself unresolved. MMAR is used here as the cleanest representative of the scale-invariant cascade structure the quantum question turns on — not as the last word.

LLM agentic AI, bounded

Classical regime-detection methods — hidden Markov models, regime-switching econometrics — operate well on quantitative inputs and are not replaced. The LLM fills the gap they cannot: reading unstructured central-bank and policy text and emitting a categorical regime signal drawn from a small, fixed, auditable set.

A hardcoded classical policy rule — not the LLM — maps that category to model parameters. The LLM never emits numbers. This confines the probabilistic, hallucination-susceptible step to a discrete, inspectable classification while the parameterization downstream stays deterministic and hand-recomputable.

Quantum compute

Positioned at a backend-agnostic tail-sampling solver to absorb its potential advantage if and when commercial viability arrives — while the system operates fully on the two classical streams today. There is no near-term quantum-advantage claim.

Any advantage the architecture would rely on is asymptotic — a claim about scaling in target precision, not about today's hardware — realizable only past a fault-tolerant threshold of unresolved location. Where any advantage exists, it lies at the sampling layer, not the loading layer, and the paper is explicit that this remains genuinely open.

Deployable today, on two classical streams.

The deep-tail confidence levels that drive capital adequacy, reverse stress testing, and tail-event preparation are exactly where the Gaussian-versus-multifractal distinction becomes consequential. The architecture runs end-to-end on multifractal mathematics and bounded LLM orchestration on commodity classical compute — its firmer half stands independent of how the quantum questions resolve.

An open question, precisely specified.

The operative hypothesis is a conjunction: that the cascade is efficiently preparable and that the deep-tail functional over it — the sampling question — might resist efficient classical contraction even at low bond dimension. Either claim without the other collapses the case. The classical experiment that would test the loading half has now been run: the cascade is not efficiently representable under the standard MPS and balanced tree-tensor-network ansatzes, reopening the loading question rather than settling it on the classical side. Two open quantum-advantage questions now stand where the architecture had expected one.

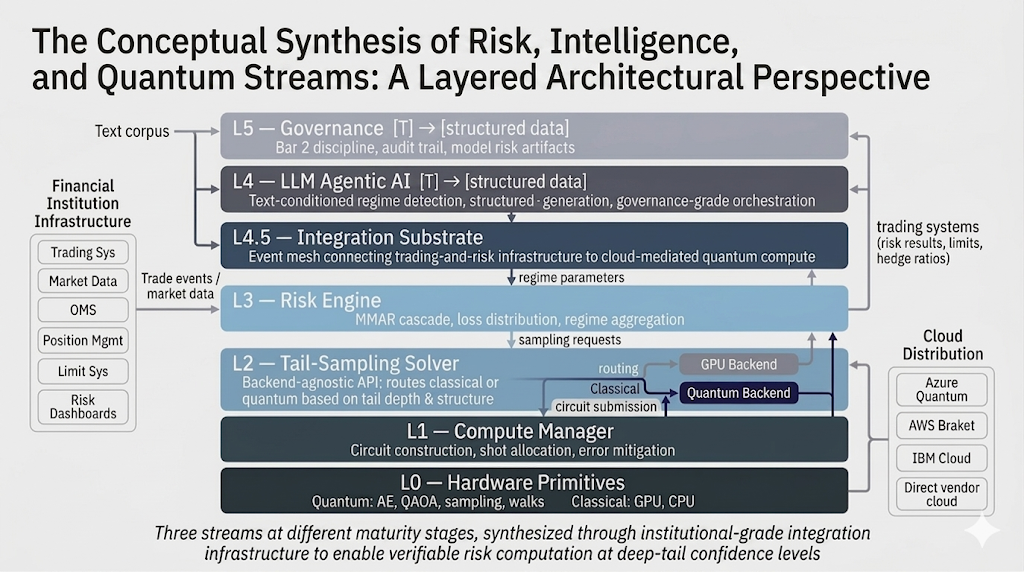

The integration substrate is the load-bearing layer.

The published quantum-finance literature systematically elides the operational layer that connects financial-institution trading and risk systems to the compute resource. That layer — not the quantum hypothesis — is this architecture's firmer contribution, alongside the structured research agenda. Financial institutions will not own quantum hardware; the economics, the operational expertise, and the hardware-roadmap volatility all argue against it. They will reach it through cloud-mediated access, and that fact has architectural consequences the literature largely ignores.

Asymmetric latency

A classical fast path serves pre-trade and intraday risk; a decoupled, asynchronous, batch-scheduled path serves the quantum-augmented analytics. There is no near-real-time quantum routing, and the architecture does not claim one.

Data residency

On-premises pre-aggregation reduces raw trade data to risk-factor exposures before any transmission to cloud compute — keeping the most sensitive data inside the institution's regulatory boundary under SR 11-7, TRIM, MAS, and FCA frameworks.

Cost as routing

Quantum execution cost scales with circuit shots, so backend routing is an economic decision taken on a batch schedule rather than per trade. Today every route resolves to the classical backend.

Two documents, one argument.

The executive summary is the entry point — self-contained, and the fastest path to the thesis, the architecture, and the research agenda. The full paper is the complete architectural treatment: the compute-stack comparison, where multifractal mathematics fits, the bounded LLM orchestration layer and its governance properties, the integration architecture, and the full open-questions research agenda.

Executive Summary

The self-contained condensation: the structural-mismatch thesis, the three streams at asymmetric maturity, the seven-layer architecture in brief, the integration substrate as the distinctive contribution, and the three decisive open questions. The blended-audience entry point for senior readers.

Quantum-Augmented Risk Management for Capital Markets: An Architectural Perspective and Empirical Loading-Layer Measurement

The complete architectural treatment. Why the question matters now; the CPU → GPU → quantum compute stack and where quantum advantage actually matters; where multifractal mathematics fits and the classical tensor-network objection engaged honestly; the bounded LLM orchestration layer with its governance properties; the seven-layer architecture; the integration architecture connecting on-premises infrastructure to cloud-mediated compute; and a structured research agenda of open questions with literature engagement and references.

Also on SSRN: ssrn.com/abstract=6874958 →

Open by design, not by omission.

Loading-tractable, yet sampling-advantaged — or neither.

Does the multifractal cascade admit a genuine quantum advantage, and if so, where? The advantage the architecture would capture exists only in a conjunction: a cascade cheap to prepare on a quantum state, yet carrying a deep-tail functional expensive to contract classically. The experiment the architecture named as decisive — a classical tensor-network measurement of the cascade’s bond-dimension scaling, requiring no quantum hardware — has now been run.

Its findingBond dimension saturates the maximum at every nonzero intermittency tested, for both multiplier laws, under the matrix-product-state and balanced tree-tensor-network ansatzes. The prior expectation that the cascade was likely classically simulable at the loading layer does not hold under these representations; the loading-layer question reopens as a candidate location for quantum advantage rather than closing. The architecture now carries two open quantum-advantage questions — loading and sampling — not one.

Where, if anywhere, does quantum help?

The loading sub-question now has a measurement: the cascade is not efficiently representable under the matrix-product-state or balanced-natural-ordering tree-tensor-network ansatzes — one classical escape route removed, no quantum alternative yet established. What stays open: whether a tree tensor network respecting the cascade’s generative structure compresses it, whether a polynomial-depth quantum preparation circuit exists, and the sampling question — do the deep-tail expectations resist efficient classical contraction. The region where a durable advantage survives is narrow and precisely specifiable.

Audit under shot noise.

Quantum execution cannot be reproduced to the decimal the way a fixed-seed classical Monte Carlo can; calibration drifts between runs. The audit unit must shift to statistical-distribution-level reproducibility under documented conditions — and whether SR 11-7 and TRIM accept that shift is itself unresolved.

The acceptance path.

Model-risk acceptance of quantum-augmented models will likely lag technical readiness by years. The demonstration sequence that would persuade supervisors is treated as an open question, not a solved problem.

One downstream consequence is worth surfacing: because the architecture reaches quantum compute through cloud-mediated access rather than on-premises hardware, and because the integration substrate is the equalizer, institutional-grade tail-risk modeling need not remain confined to tier-one technology firms. As commercial viability emerges, the framework is in principle accessible to a far broader range of institutions — mid-tier banks, regional broker-dealers, pension funds, sovereign wealth funds, insurance reserving operations, and central clearing counterparties.

The author welcomes engagement, critique, and collaboration on the open questions the paper raises.